Like usual, the Intelliversity blog gives you a practical tip or two for success as a Vision Master (a success-hack) and some general principles for vision masters, mostly around funding. It’s all about being unconventional as a founder, because “If you behave like everyone else, you’ll get the same results as everyone else.”

You may wish to view this overview video first

You can listen to the podcast of this post below:

In the case of innovative startups, only 5% get funded (outside friends and family), and only 10% ever succeed enough to pay back their investors. That’s what “everyone else” gets. But you don’t have to be like “everyone else.” Getting much better results than “everyone else” is what this blog and Intelliversity is all about. So you have to do things differently than everyone else. That’s why we give unconventional tips and principles. Now, onward ...

Imagine your home is on fire. There’s a certain sequence of steps you’ve got to take, and you may instinctively take, that handle priorities in the right order. If you do these steps in the right order, not only will you and your family survive, but you’ll be able to improve your life after the fire is out. The same principles apply to the COVID-19 pandemic and related economic dislocation, except that the steps are not as obvious. Let’s start with the fire situation and then graduate to how these lessons are applied to saving and growing your business after a crisis.

There are three steps to take if your house is on fire.

- Survive: Get yourself and your loved ones out, alive (short-term response)

- Stabilize: Make sure you and your family are going to be safe over the months needed to rebuild (mid-term response)

- Strengthen: Take advantage of the situation to improve your family relationships, your career and your business (long-term response)

The same steps apply to any crisis, a disease pandemic for example:

As you’re working through steps 1 and 2, keep in mind that step 3 is coming soon. Keep in mind that you don’t have to just get back to normal after the crisis; that you can use this crisis, any crisis, to strengthen every aspect of your life beyond what was normal. I’m willing to assert that crisis is THE best opportunity to strengthen family, career, and business.

Note that you avoid placing blame during steps 1 and 2. Stage 3 is where you might want to make plans to prevent fires in your home (and to improve your response to a fire), which may involve finding out the causes of the disaster, and the causes of errors in handling the fire. But, even in Step 3, only part of the time is spent on discovering causes and placing responsibility.

Most of the time is spent making changes so that your future is brighter because of what you learn from the disaster. This includes taking the opportunity for greater intimacy with family and friends. For those of you who have the role of bringing home the bacon, this is also an opportunity to put aside petty reactions, emotional breakdowns, and personal vices, and elevate your commitment to protecting your family and furthering your career and business.

You may find yourself delegating who is responsible for each of these steps to different people, each with specialized skills and motivations. For example, the firemen may handle #1, your spouse may handle #2, and you may handle #3. Whatever fits their talents and motivations.

So now let's see how these ideas apply to the present COVID-19 crisis, as it applies to your young innovative business:

-

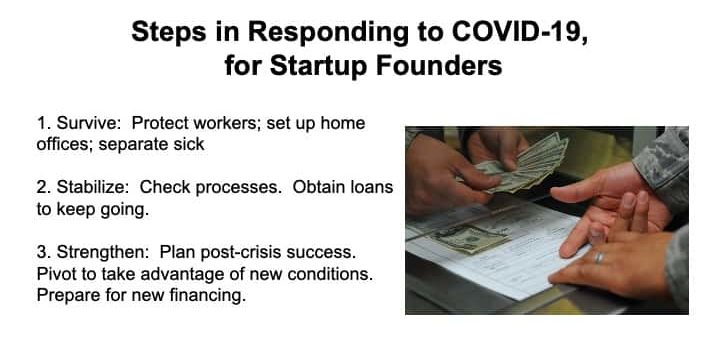

Survive: Take care of anyone sick. Enforce social distancing on the job and set up home offices wherever possible. This is the step where you just focus on keeping your business alive short-term. These tips come from the SBA:

- Actively encourage sick employees to stay home

- Separate sick employees

- Emphasize staying home when sick, respiratory etiquette and hand hygiene by all employees

- Perform routine environmental cleaning

- Advise employees before traveling to take certain steps

- Check the CDC’s Traveler’s Health Notices for the latest guidance and recommendations for each country to which you will travel. Specific travel information for travelers going to and returning from designated countries with risk of community spread of Coronavirus, and information for aircrew, can be found on the CDC website.

Additional Measures in Response to Currently Occurring Sporadic Importations of the COVID-19:

- Employees who are well but who have a sick family member at home with COVID-19 should notify their supervisor and refer to CDC guidance for how to conduct a risk assessment of their potential exposure.

- If an employee is confirmed to have COVID-19, employers should inform fellow employees of their possible exposure to COVID-19 in the workplace but maintain confidentiality as required by the Americans with Disabilities Act (ADA). Employees exposed to a co-worker with confirmed COVID-19 should refer to CDC guidance for how to conduct a risk assessment of their potential exposure.

-

Stabilize: Make sure that teamwork and business processes continue to work. Obtain emergency and payroll financing. This is where you begin to think about staying in business for the next few months (mid-term). Reduce burn rate so that your available funds will last six more months than you had planned. However, avoid layoffs by obtaining payroll financing.

- Capital Access – Incidents can strain a small business's financial capacity to make payroll, maintain inventory and respond to market fluctuations (both sudden drops and surges in demand). Businesses should prepare by exploring and testing their capital access options so they have what they need when they need it. See SBA’s capital access resources.

- Workforce Capacity – Incidents have just as much impact on your workers as they do your clientele. It’s critical to ensure they can fulfill their duties while protected.

- Inventory and Supply Chain Shortfalls – While the possibility could be remote, it is a prudent preparedness measure to ensure you have either adequate supplies of inventory for a sustained period and/or diversify your distributor sources in the event one supplier cannot meet an order request.

- Facility Remediation/Clean-up Costs – Depending on the incident, there may be a need to enhance the protection of customers and staff by increasing the frequency and intensity by which your business conducts cleaning of surfaces frequently touched by occupants and visitors. Check your maintenance contracts and supplies of cleaning materials to ensure they can meet increases in demand.

- Insurance Coverage Issues – Many businesses have business interruption insurance; Now is the time to contact your insurance agent to review your policy to understand precisely what you are and are not covered for in the event of an extended incident.

- Changing Market Demand – Depending on the incident, there may be access controls or movement restrictions (voluntary or mandatory) which can impede your customers from reaching your business.

- Marketing – It’s critical to communicate openly with your customers about the status of your operations, what protective measures you’ve implemented, and how they (as customers) will be protected when they visit your business. Special promotions may also help incentivize customers who may be reluctant to patronize your business.

- Plan – As a business, bring your staff together and prepare a plan for what you will do if the incident worsens or improves. It’s also helpful to conduct a tabletop exercise to simulate potential scenarios and how your business management and staff might respond to the hypothetical scenario in the exercise. For examples of tabletop exercises, visit FEMA’s website at https://www.fema.gov/emergency-planning-exercises

-

Strengthen: Plan for success after the crisis, including pivot if needed. This is where you plan to take advantage of the crisis to improve your business.

- Think higher revenues post-crisis. You may have opportunities for new products/services or even a major pivot in the business model.

- Strengthen your advisory board and team. Plan for a new round of financing. Talk to advisors, including us, about what’s possible. Then start talking to investors as soon as they’re available.

- This is where you think long-term. Remember that if you start working on this level now, you’ll have an advantage over others that are stuck at levels 1 and 2.

You may find yourself delegating who is responsible for each of these steps to different people, each with specialized skills and motivations. For example, a trusted assistant might handle #1 (under your leadership), your operations manager (execution master) might be responsible for #2, and you may handle #3 personally. as your company’s Vision Master.

You may have to kick yourself in the pants to get your head out of the news and back into action. But this is an emergency and you must relate to it like it must be done NOW.

Keep looking over the horizon to the post-crisis era, the strengthen stage of crisis response. Remember that you can use any crisis to strengthen family, career, and business if you deliberately work at it. A crisis can bring out the worst in your family and teams - blaming others, defending, power plays, anger, withdrawal, denial, self-justification, you name it. Lead from the calm and confident belief that the future will be brighter if we stay calm and see that hanging together is better than falling apart. The leader with the further vision and who aims for the widest impact will pull everyone else out of the mud. Be that leader, vision master.

As vision master, getting past your own emotional reactions is key to maintaining focus on the future and pulling everyone out of the mud. Remember, the most reliable antidote to emotional reaction is to focus on the facts. Facts are nature’s tranquilizer. Your immediate steps for survival and stability must be based on clear-headed mindfulness, paying attention to what’s really going on.

Even your future vision to strengthen the family and business must be based on facts - specifically a fact-based plan to get you there. Don’t be a visionary; be a Vision Master. A visionary sees the future; a vision master makes the future and making the future requires a plan, a fact-based plan. A vision without a plan is a mirage. A vision with a fact-based plan is literally further down the road.

Now onward to a specific action you can take today, this weekend, or at the beginning of the coming week -- to get some additional funding right away to keep the business afloat.

Get an application from your bank now for a one-time COVID-19 pandemic PPP loan. This HAS to be done through an SBA-approved lender, not directly to the SBA. Banks are flooded with applications already, so get yours in quickly in the next few days before funds run out.

If your bank doesn’t provide SBA PPP loans now, then go to a Preferred SBA Lender. Preferred Lenders have underwriting authority to make a final lending decision, which will speed the process for you.

Get help from your CPA and CFO to maximize loan and maximize how much is forgiven. Give yourself (or your team) at least a full day to get this done, as it requires some thought to compute the loan amount allowed and to collect the supporting documents.

If your CPA doesn’t have a well-defined program to help you apply for the SBA PPP loan, check out this program: https://www.youtube.com/watch?v=IT52HFCNC88

When planning for the post-crisis market, make changes to take advantage of the new market over the next five years. Be optimistic. Think like Warren Buffett. A crisis is the best opportunity to gain an advantage. For example, this may be the best chance to buy up slower-moving competitors or companies with overlapping markets, where their management can’t survive without your bold leadership and vision and innovative thinking. And it may be the best chance to introduce new products or services or alter your business model, to best assist people and businesses in a recovering world. Be innovative.

Investors are turning away from the pre-crisis default-dead companies that required round after round of funding to stay alive, always relying on a greater fool to fund the next round. Present yourself as default-live, meaning that the next round is the last one you’ll need to get to cash-flow positive. Further rounds of funding will be optional to increase scale, but not required for survival.

Investors at this time are more skeptical and fearful than ever. Yet they do think like Warren Buffet and want to take advantage of the crisis of fewer competing investors. They will push down on your valuation. To maintain the valuation, you expect and deal with the extra layer of fear, be sure to carefully address and mitigate all risk factors. Ask yourself “Most new companies fail. What factors will cause us to fail? How have I mitigated these factors?”

Then finally, when talking with investors, sell trust in you personally ahead of selling the opportunity. Remember they can’t see your ideas while they’re blinded by their fears.